Dissecting trades using R-Multiples

In this post I explore analysing your trading outcomes using R-Multiples for truly comparative and fair inter-trade results.

Only one point is certain when you take a trade: the point at which you enter. Anyone can place a trade at the click of a button – that’s easy – but the exit point is what cements the result. In many ways, choosing the exit point is what makes trading so difficult because you, the trader, are solely responsible for it. The market will move regardless of your insignificant involvement; it is your job as a trader to hitch a ride and get out when you feel that the timing is right. And so, exiting becomes a mental game that the trader plays with himself (or herself!).

Determining the “perfect” exit point, where momentum is waning or where a support or resistance level is set, is a function of your trading process and system. Your trading process and system also give you the framework within which to analyse and understand your performance. Building this framework includes deciding not only when to enter and (manually) exit, but also where to place a target and a protective stop (or stop-loss). These effectively determine the boundaries of your trade. The same protective stop that defines your risk also amounts to your admission fee, so to speak, to enter the market and participate in the trade. If things go your way, the market waives that admission fee. If they don’t, the market keeps the fee and you get out before things get worse.

The lifeblood of your trading journey is the capital in your trading account. Your first goal is to protect it, and your second goal is to grow it. By protecting it, you ensure that you stay in the game long enough to find opportunities that give you a chance to grow it. Hence, the protective stop, which gets you out of the trade, minimises the capital loss that you are willing to risk to participate in the trade. In order to achieve both goals (and ultimately make a profit), you need to gain more than you lose, so it makes sense to analyse your performance as a function of what you are willing to risk to make a profit. What does this look like in practice? Let’s look at an example that breaks down the anatomy of a trade.

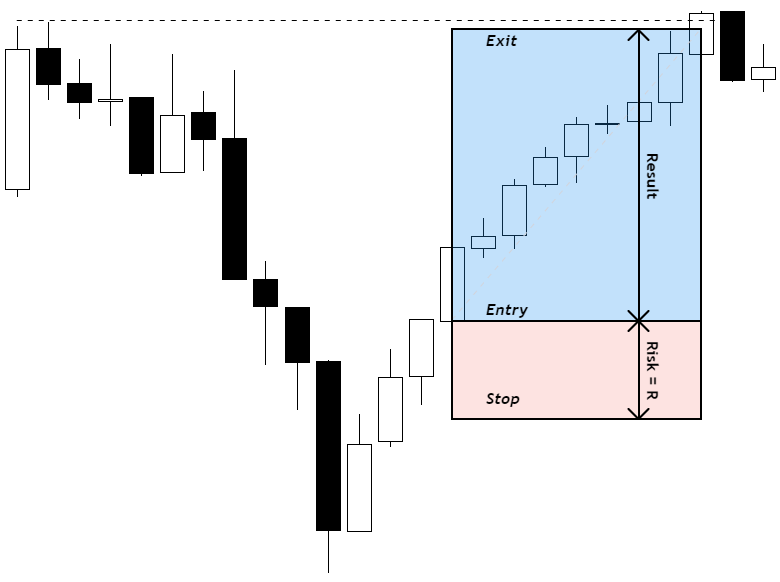

First, let’s set the scene: suppose you are watching your favourite market to trade. Your framework has determined that you should buy the asset to go long (i.e., your framework predicts a higher probability of prices going up than down), and you decide that you want to target the previous highs. You define an entry point and determine a logical stop level (i.e., the threshold at which your expectation of prices going up is proven to be incorrect). For example, you could decide that this threshold should be where the previous candle’s low is broken. As it happens, this stop level is 3 points away, while your target (i.e., the previous high) is 12 points away. This trading opportunity therefore represents a risk-to-reward ratio of 4 (i.e., 12 divided by 3). So, if you risk 1% of your trading capital, you stand to make 4% of your trading capital if the price reaches your target and you exit the trade accordingly. Once you have determined the boundaries of your trade, you open a position and enter the market.

After some time, your framework’s expectations are fulfilled; prices go up and reach the previous highs, you exit the trade at your intended target, and you make a 4% profit. This is the ideal outcome. Let’s translate these results into the R-Multiple method of analysing trades.

As I explained above, your stop-loss defines your risk, and so the distance to stop-loss level is represented by R. In this case, the value of R is 3, because your stop-loss level was 3 points away from your entry point. Dividing your profitable (“+”) result of 12 points by the value risked (R = 3) yields a trading outcome of +4R.

Now you might be wondering what the point is for all of this basic mathematics. The benefit of the R-Multiple method is that it gives traders a way of measuring performance irrespective of the actual monetary value of the trade, or the amount gained (or lost). All that matters is how the trade performed relative to what you were willing to risk to participate in the trade. In the R-Multiple format, the outcome of this trade is represented by +4R, regardless of whether you risked 1% of your trading capital or 10% or a simple, straightforward $1. However, the R-Multiple is not to be confused with the risk-to-reward ratio of a trade. Risk-to-reward is defined at trade entry but a trade’s R-Multiple is purely a function of the outcome.

Let's use another example to showcase this.

Trader A has an account size of $5,000 and Trader B has an account size of $10,000. Trader A decides to risk 1% ($50) of his account in a trade, whereas Trader B decides to risk 2% ($200). Both Traders follow the same trading process to determine their entry and target.

Once both Traders’ positions are closed out, Trader A makes $150 whereas Trader B makes $200. From a purely monetary value perspective, Trader B would be seen as having performed better, because a $200 profit is greater than a $150 profit. However, a different picture is painted once we consider the risk that each Trader was willing to take to participate in the trade, and what each Trader produced.

Trader A risked $50 (which is Trader A’s R) to make $150. In R-Multiple terms, Trader A produced an outcome of +3R (i.e., a profit of 3 times the amount risked, or 3 x $50 = $150).

Trader B risked $200 (which is Trader B’s R) to make $200. In R-Multiple terms, Trader B produced an outcome of +1R (i.e., a profit of 1 times the amount risked, or 1 x $200 = $200).

Now we have a fair comparison of the Traders’ performances, being +3R vs +1R. Even though Trader B exited the trade with more money, Trader A performed better from the same entry point, producing 3 times what he risked instead of 1. So what could have happened to produce the different results? Trader B may have been negatively influenced by a variety of factors and did not extract the optimal value from the market even though both Traders were using the same trading process.

Naturally, the same R-Multiple format can be used to assess negative results.

Say you enter a trade by risking $50, but the market moves against you and your stop-loss level is reached, meaning you lose all $50. In this case, your R-Multiple would be -1R because a loss-making (“-”) result of $50 divided by the amount risked (i.e., R = $50) yields -1.

However, if you enter a trade by risking $50, but you are stopped out at $100, your R-Multiple would be -2R, meaning that you initially risked $50 but ultimately lost $100. Therefore, if you ever have an R-Multiple that is less than -1R (e.g., -2R, or -1.5R, etc.) it means that you lost more than you initially wanted to risk.

For the purposes of analysis, the value of R is fixed at the point of trade entry. In the case of a long trade (i.e., you buy the asset, expecting the price to go up), if you move your stop-loss level higher as price runs higher so that you can lock-in profits (or smaller losses), the value of R does not change for that trade. Similarly, if you commit a grave trading atrocity and move your stop-loss down to avoid being taken out, you open yourself up to larger losses but the value of R does not change.

The real beauty of the R-Multiple method emerges when you start analysing more than one trade, and then a series of trades. This process is explained in detail by Van K. Tharp in his book Super Trader, which I highly recommend. It is this book that introduced me to trade analysis using R-Multiples.

In summary, the R-Multiple method of trade analysis allows for complete and fair inter-trade comparisons. Although each trade’s R-value may be different (whether it be a monetary value or risk percentage), the units of measure are removed when converting each trade into its own R-Multiple. This is extremely useful for comparing your own trades and tracking your performance over time as it standardises the results. This is true even if the monetary value of the capital you risk per trade changes, which can happen especially if you use a percentage risk model and the value of your trading capital changes.

As you enter (and exit) more and more trades over time, you will develop an R-Multiple distribution for your trading process and performance. This distribution can then be used to find performance patterns, calculate average R-Multiples for winning and losing trades, as well as your standard deviation in order to determine your trading consistency. The R-Multiple distribution will show you the true performance of your trading process.

This is a process I have followed during my trading journey (and you will see I have been using it to analyse my trades in earlier posts on my blog). It has provided me with a fair and very useful comparative analysis for exploring my trading results, process, and performance.

That being said, the R-Multiple method might not work for everyone. All traders will take their own approach to trading, and understand their results in a unique way. I only hope that this adds another valuable tool to your trading analysis kit and that some may find it helpful to quantify their trading edge.

~Alessandro :)